This article is an on-site version of our Unhedged newsletter. Sign up here to get the newsletter sent straight to your inbox every weekday

Good morning. Today we all hold our breath, awaiting the Federal Reserve’s statement at 2pm Eastern Time and the press conference that follows. There has been speculation that officials might raise the possibility of a 50 basis point rate increase at the March meeting, or of a 25bp rise at all seven of its remaining meetings this year. Either would spook the market, and both strike us as wildly unlikely. Mostly we will be listening for hints about whether the Fed might shift its balance sheet into run-off mode as soon as bond buying stops in March.

In the meantime, more on the US stock market’s gymnastics, and a few thoughts on the increasingly frightening situation on the Ukrainian border.

Email us: robert.armstrong@ft.com and ethan.wu@ft.com.

Two bright spots on a bad day for stocks

We will spare you the play-by-play on another batty day in US equities. But two things strike us as worth noting. First, although it sold off again, the market is still making distinctions. It still favours shares that are sensitive to rates and economic growth. Witness the KBW Bank index, which ended the day in the green.

Second, Tuesday brought a reminder of what has powered US equities for so long, and could keep powering them: really good earnings. American Express came out with a big fourth-quarter beat, crushing analyst expectations. It reported record quarterly spending fuelled by young consumers. Spending on its card network in the fourth quarter was 11 per cent above pre-pandemic 2019, and the company expects more strong spending this quarter. The stock closed up close to 9 per cent.

The real test this year: do we have enough Amex-es to offset tighter financial conditions?

Russia-Ukraine conflict: a tail risk, but a big one

While most investors are focused squarely on the volatility in equity markets, another, more significant story continues to unfold: tensions on the Russia-Ukraine border. We will not speculate on the probability that the brinkmanship devolves into open conflict, as opposed to serving as the necessary prelude to a diplomatic solution — except to note two things.

First, every expert we spoke to saw a low likelihood of anything that could be described as invasion or territorial annexation, but that the economic consequences of any such event would be significant (to say nothing of the political and humanitarian consequences).

Second, local currency and bond markets reflect worries, but not panic, about the situation. Ukrainian dollar bonds that mature in the next year or so are trading near to par. Those with longer maturities have seen their discount grow over the past two months, but not to desperation levels:

Similarly, while the rouble has not collapsed in recent months, it has not strengthened as oil prices have shot up, as it has in the past. Political risk has depressed the Russian currency (note the inverted rouble/$ scale):

The two main mechanisms by which a deepening conflict would affect regional and global markets are international sanctions against Russia, and rising prices of natural gas and oil, if Moscow were to restrict outgoing supply to Europe.

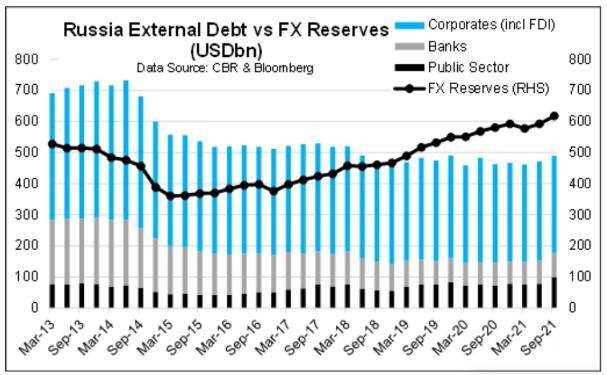

One factor that is relevant to Russia’s ability to withstand sanctions, and its willingness to use its oil and gas for leverage, is its high level of what we might call financial insulation. This has been built up since 2014, when sanctions bit following the annexation of Crimea.

Russia has bolstered itself against potential sanctions. As Simon Quijano-Evans, Gemcorp’s chief economist, puts it:

Russia has become more introverted, it has lower external debt and higher FX reserves, and one of the lowest public debt to GDP ratios in the world — they need the outside world less now.

Here is a chart from Quijano-Evans, showing Russia’s rising reserves of foreign currency, as well as falling levels of external debt at its banks and corporates:

The country’s combination of low government debt and low dependence on state spending is unique and provides room for manoeuvre:

This is not to say sanctions would be painless. Its stock market and sovereign bonds could take even more of a beating than they already have (eastern European stock and bond markets would feel the pain as well). But only the most extreme sanctions could force Russia into a financial crisis. And there are two reasons to think that the most severe sanctions — for example, making it very difficult for the country’s banks to get access to external dollar funding — are unlikely to be imposed. The first, as explained by Edward Glossop, Aberdeen Standard economist, is that:

There is a bit of a wedge between the US and the EU on the sanctions response, because the US is more hawkish, and the EU requires a unanimous vote. There is always a few member states that want to soften the response — you would need to get a very strong military expansion [by Russia] to get strong sanctions against Russian banks.

The second issue is that sanctions will not just hurt Russia. Data from the Bank for International Settlements shows that international banks, (including their Russian subsidiaries) have some $121bn in assets that are owed to them by Russian entities. On the other side of the ledger, international banks have some $128bn in loan and deposit funding owned by Russian entities. Squeeze the Russian financial system too hard, and western banks, particularly in Europe, will start to squeal.

That leaves the question of Russia tightening the taps on its oil and gas exports. The big risk here is that this could potentially have a stagflationary effect, that would in turn knock global equity and bond prices. As Nanette Abuhoff Jacobson, a strategist at Hartford Funds, put it to us:

If oil prices spike to over $100 a barrel, that’s going to be a shock to supply, but also it’ll feed into a huge tax on consumers. So again, a low-probability risk, but definitely a stagflationary type of risk.

Inflation is already a political issue. Consumers’ perception of gas prices [among other things] is what is weighing on consumer sentiment. That is the reason consumer sentiment is so weak.

Quijano-Evans sees open conflict leading to higher energy prices and lower confidence. Both would dampen economic activity, and force banks that are tightening policy now to reverse course. The result could be stagflation.

As the master of setting out dire consequences, the economist Nouriel Roubini, put it to us in an email:

If a full invasion of Ukraine by Russia does occur . . . of course the largest hit to growth and risky assets would be in Ukraine and Russia. But there are global implications too: the supply of gas to Europe would be partially curtailed as EU/Nato retaliates with trade/financial sanctions and the Nord Stream 2 pipeline may never come on line. Thus, elevated natural gas prices will become even higher during peak winter heating season in Europe. That will have spillover to oil prices given the link between the two markets. Thus, at the margin US and EU and global inflation goes higher and growth lower, a stagflation-lite outcome.

What are investors to do? Edward Al-Hussainy of Columbia Threadneedle says that the only positive bet one can make is that open war can be avoided, and that Ukraine bonds and the rouble will rise sharply. For those without confidence in that outcome, he says various hedges are available: get long the bonds of oil-exporting countries in the Middle East, and short those of energy importers such as Turkey. Buy high-yield bonds of energy producers in the US shale patch. Short European high-yield corporates, while buying German long bonds, as a hedge against recession there.

But the biggest risk posed by war, however big or small, is not stagflation. It is more war, especially in a world reeling from a pandemic and where other political tensions are festering. Here again is Quijano-Evans:

The question we should be asking ourselves, how can this be happening? There has to be some sort of political or diplomatic solution that can be reached. We just came out of a global pandemic, a worse situation, in a way, than 1918. The world is so tired, it cannot take another conflict. We should be thinking about the connotations for other global conflicts.

Roubini spells out the worst-case scenario:

A Russian invasion of Ukraine may also make the other three revisionist powers challenging the US/western order more aggressive: China in the South China Sea and Taiwan (Chinese incursions in Taiwan airspace have recently increased); Iran may be less willing to negotiate a new [nuclear agreement] as the US becomes more desperate to get one to calm oil markets and eventually Israel may strike Iran; and North Korea has already increased the rate at which it launches provocative missiles.

These risks are at the extreme edge of the probability distribution. But they should not be ignored. (Armstrong & Wu)

One good read

If you’re on Twitter, you might’ve seen the new non-fungible tokens profile pictures, made distinct by hexagonal borders around your avatar. Why Twitter did it, from Scott Duke Kominers of Harvard Business School.

Recommended newsletters for you

Due Diligence — Top stories from the world of corporate finance. Sign up here

Swamp Notes — Expert insight on the intersection of money and power in US politics. Sign up here